Cash flow forecasting helps small businesses stay in control of their finances. It predicts when money will enter and leave your business, ensuring you can cover expenses like payroll, rent, and inventory without surprises. This guide breaks down the essentials:

- Why it matters: Poor cash flow management causes 82% of small business failures. Yet, 92% of owners rely only on their bank balance to make decisions – an approach that risks financial trouble.

- How it works: Analyze past data (sales, expenses, payment terms) to estimate future inflows and outflows. The goal? Know your net cash flow and prepare for challenges like late payments or seasonal dips.

- Types of forecasts: Use short-term (1–3 months) for immediate needs, medium-term (3–12 months) for planning, and long-term (1–5 years) for growth decisions.

- Methods: The direct method tracks cash as it moves in and out, ideal for short-term needs. The indirect method adjusts profit figures to show cash trends, better for long-term planning.

- Steps to create one: Gather past financial data, estimate inflows and outflows, calculate net cash flow, and update regularly.

Pro tip: Use tools like QuickBooks to automate forecasts, or work with advisors for added accuracy. Weekly updates and scenario planning (best, worst, and average cases) can help you spot and address cash gaps early.

Cash flow forecasting isn’t just about survival – it’s about making informed decisions and building financial stability.

How to Create a Cash Flow Forecast (in under 20 minutes) {FREE TEMPLATE}

sbb-itb-c53a83b

Types of Cash Flow Forecasts

Cash flow forecasts can vary based on their timeframe and purpose, ranging from ensuring next week’s payroll is covered to planning for long-term business growth.

Short-Term Forecasts

Short-term forecasts usually cover one to three months and focus on immediate cash needs. They detail transactions like customer payments, supplier invoices, and payroll schedules. For small and medium-sized businesses (SMEs), a 13-week forecast is common, as it provides a clear view of the upcoming quarter. In situations where cash is tight, weekly updates can help identify gaps six to eight weeks in advance, giving businesses time to adjust spending or secure additional funding.

While these forecasts are essential for managing daily operations, medium-term forecasts take a broader approach.

Medium-Term Forecasts

Medium-term forecasts extend over three months to a year and are designed for strategic planning. They help businesses prepare for seasonal changes, plan hiring schedules, and strengthen loan applications by showcasing financial stability. Instead of tracking every single transaction, these forecasts group data into broader categories like total revenue, payroll, and marketing expenses. Many businesses use a rolling 12-month forecast, which adds a new month as the previous one ends, ensuring projections stay aligned with current trends. Monthly updates keep these forecasts practical and actionable.

For decisions that go beyond seasonal adjustments, long-term forecasts provide a roadmap for growth.

Long-Term Forecasts

Long-term forecasts, looking one to five years ahead, guide major decisions like expanding to new locations, purchasing equipment, or pitching to investors. These forecasts focus on overall cash flow rather than individual transactions. They are often based on projected net income, adjusted for non-cash items like depreciation. Because they rely on assumptions about market trends and regulatory changes, their accuracy can vary. To stay relevant, update these forecasts quarterly or annually, and document key assumptions to make future revisions easier.

Cash Flow Forecasting Methods

Direct vs Indirect Cash Flow Forecasting Methods Comparison for SMEs

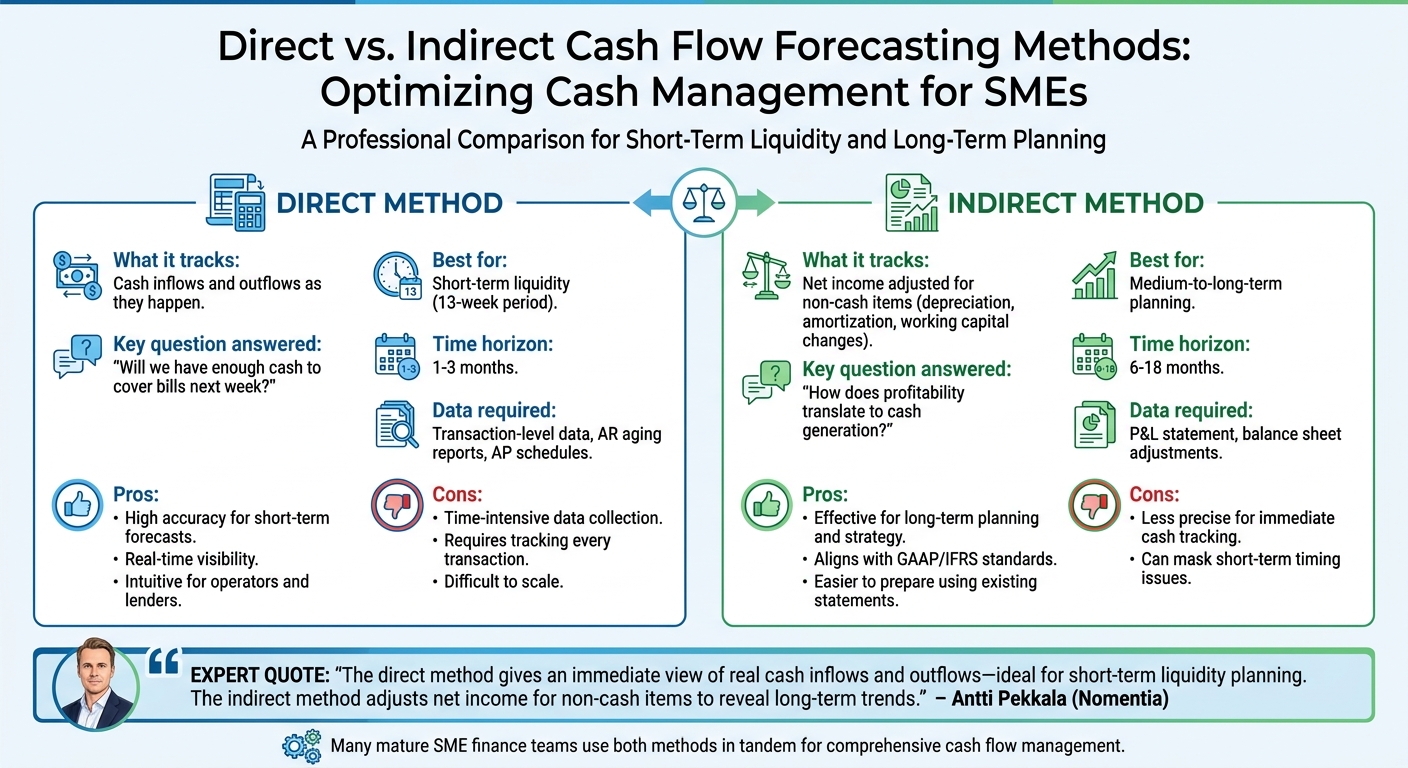

After determining your forecasting timeframe, the next step is deciding how to structure your forecast. Small and medium-sized enterprises (SMEs) generally rely on one of two approaches – direct or indirect. Each method serves a distinct purpose and addresses different aspects of your business’s cash flow.

Direct Method

The direct method tracks cash inflows and outflows as they happen. Payments from customers are recorded when they reach your account, supplier payments are noted when invoices are settled, and payroll is logged when the funds clear.

This method is ideal for managing short-term liquidity over a 13-week period. It answers the pressing question: "Will we have enough cash to cover our bills next week?" For SMEs operating with tight cash reserves, a 13-week cash flow forecast is often considered the gold standard. Brad Jungers, Founder & CEO of CFO Insights, emphasizes the importance of accurate financials, stating, "your interest expense is going to go down" when lenders trust your numbers. However, this method can be labor-intensive, requiring detailed transaction-level data from accounts receivable aging reports and accounts payable schedules.

On the other hand, the indirect method focuses on financial statement adjustments to analyze long-term cash flow trends.

Indirect Method

The indirect method begins with net income from your profit and loss statement and adjusts for non-cash items like depreciation, amortization, and changes in working capital. Instead of logging individual transactions, this approach reconciles discrepancies between your bank balance and reported profit. It is the go-to method for external financial reporting under GAAP and IFRS, making it a favorite among boards, investors, auditors, and tax professionals.

This method is better suited for medium-to-long-term planning, typically spanning six to 18 months. While it may lack precision for immediate cash flow tracking, it excels at identifying long-term trends and clarifying how profitability translates into cash generation. Antti Pekkala from Nomentia explains:

"The direct method gives an immediate view of real cash inflows and outflows – ideal for short‑term liquidity planning. The indirect method adjusts net income for non‑cash items to reveal long‑term trends".

Because it relies on existing financial statements, the indirect method is generally easier to prepare.

Direct vs. Indirect: Pros and Cons

Both methods come with their own strengths and limitations, and many mature SME finance teams use them in tandem. The direct method provides detailed, real-time insights into daily collections and payments, while the indirect method offers a broader narrative for strategic planning, valuation, and compliance. To simplify workflows and avoid duplicating efforts, many organizations integrate both methods using shared Chart of Accounts mappings and automated data feeds from their ERP or accounting software.

| Method | Pros | Cons |

|---|---|---|

| Direct | High accuracy for short-term forecasts; real-time visibility; intuitive for operators and lenders | Time-intensive data collection; requires tracking every transaction; difficult to scale |

| Indirect | Effective for long-term planning and strategy; aligns with GAAP/IFRS; easier to prepare using existing statements | Less precise for immediate cash flow tracking; can mask short-term timing issues |

Selecting the right method – or combining both – ensures SMEs can manage cash flow with clarity and confidence.

How to Create a Cash Flow Forecast

Creating a cash flow forecast doesn’t require a degree in finance – just a commitment to gathering the right data and applying realistic assumptions. Let’s break it down into five straightforward steps that turn past financial data into a tool for managing your cash flow effectively.

Step 1: Gather Historical Data

Start by pulling together three to six months of bank statements. These will show the actual timing of deposits and withdrawals, which may not always align with what your accounting software suggests. Additionally, grab your Income Statement, Balance Sheet, and past Cash Flow Statements to understand your revenue and expense patterns.

Pay close attention to your Accounts Receivable aging reports. These reports reveal how long it really takes customers to pay, which might be longer than the invoice terms indicate. For example, if your invoices state "Net 30" but payments typically come in 45 days, that delay impacts your cash availability. As David White from Relay points out:

"Cash and profit follow different timelines and that gap is what catches most business owners off guard".

Don’t forget irregular expenses like annual insurance premiums, quarterly taxes, and license renewals. Look at two to three years of revenue data to spot any seasonal trends. Also, gather detailed payroll records (including taxes and benefits) and Accounts Payable information, noting vendor payment terms. Your forecast should reflect the actual timing of bank transactions rather than just accounting entries.

When determining your starting balance, include only liquid cash – like funds in checking, savings, or money market accounts – and exclude pending deposits or available credit lines.

Step 2: Estimate Cash Inflows

Once you’ve reviewed historical data, shift your focus to forecasting cash inflows. The key here is to track when money will actually hit your account – not just when sales are booked. For instance, a $50,000 sale might close today, but if it takes 60 days to collect, that delay matters – especially when payroll or other obligations are due.

Use your Accounts Receivable data to calculate average collection times for different customer segments. If enterprise clients typically pay in 60 days instead of the expected 30, include that in your forecast. Break down inflows by source, such as customer payments, loans, or investment capital, and adjust for seasonal trends.

Be conservative with your estimates. Avoid overly optimistic assumptions and aim for realistic accuracy – targeting 80–90% precision for the current month and 70–80% for the next two to three months.

Step 3: Estimate Cash Outflows

Now, figure out how much cash will flow out. Divide expenses into three categories:

- Fixed costs: These include rent, software subscriptions, and base payroll.

- Variable costs: Think shipping, raw materials, or commissions, which fluctuate with sales.

- Irregular expenses: Items like annual insurance, quarterly taxes, or equipment purchases.

For irregular costs, list out each payment and assign it to the month it’s due to avoid unexpected shortfalls. It’s also wise to set aside 10–20% of your monthly expenses for a contingency fund to cover surprises like repairs or legal fees.

Step 4: Calculate Net Cash Flow

The formula is simple: Total Cash Inflows – Total Cash Outflows = Net Cash Flow.

To find your Closing Cash Balance, start with your opening balance, add inflows, and subtract outflows. For short-term management, calculate this weekly over a 13-week period. For long-term planning, monthly projections over 12 months work well. The closing balance from one period becomes the starting balance for the next.

If your closing balance dips below your target reserve – typically one to two months of operating expenses – you’ve identified a potential cash crunch. Run different scenarios to prepare for challenges. For example, what happens if your largest customer delays payment by 30 days? Or if sales drop 15% next quarter? These “what-if” exercises help you plan ahead.

Step 5: Review and Update Regularly

A cash flow forecast isn’t a one-and-done task. Regular updates ensure your projections stay relevant as market conditions, supplier costs, and customer behaviors shift.

For a 13-week forecast, update it weekly – ideally at the start or end of the workweek. For a 12-month forecast, monthly updates should suffice. Use a rolling window approach, adding a new week to your 13-week forecast as each week passes to maintain a continuous three-month view.

Conduct variance analyses to compare actual results with your projections. Use any discrepancies to refine your assumptions and improve accuracy over time. As Brad Jungers, Founder & CEO of CFO Insights, highlights:

"When they trust your financials, your interest expense is going to go down".

Regular reviews also act as an early warning system. Spotting potential cash flow issues six to eight weeks in advance gives you time to secure credit or accelerate collections if needed.

Best Practices for Cash Flow Forecasting

Creating accurate cash flow forecasts isn’t just about crunching numbers – it’s about adopting a disciplined and strategic approach. Here are three essential practices that can help small and medium-sized enterprises (SMEs) move from guesswork to reliable forecasting.

Use Scenario Planning

Avoid relying on a single forecast. Instead, develop three scenarios: a base case (your most likely outcome), an optimistic case (strong growth), and a pessimistic case (reduced sales or delayed payments). This method transforms your forecast into a set of boundaries, showing how your cash flow holds up under varying circumstances.

Dive into key "what-if" questions. For instance, what happens if your biggest client delays payment by 30 days? Or if a supplier increases prices by 8%? These scenarios help you prepare for potential cash gaps.

Andrew Lokenauth, writer of "thefinancenewsletter", shared in April 2026 that updating rolling forecasts every Monday improved his forecasting accuracy by 40% – and it only took him two hours each week.

Keep your scenarios grounded in reality. Your pessimistic case shouldn’t be overly dramatic, like a total collapse, but instead focus on plausible challenges – such as losing a major customer or experiencing a three-month contract delay. Limit your scenarios to three to five for clarity, and document the assumptions behind each one. For example, you might note, "Assumed 5% revenue growth due to a new product launch." This practice helps you pinpoint potential cash gaps weeks in advance.

Integrate Forecasting with Financial Tools

Once you’ve developed multiple scenarios, the next step is ensuring your data stays up to date. Manual spreadsheets often lead to errors and, by the time they’re updated, the data is already outdated.

Link your forecasting process to accounting software like QuickBooks or Xero, as well as your bank feeds and payroll systems. Automating these connections reduces manual data entry and ensures real-time insights into your cash flow.

Jeffrey Zhou, founder of Figloans, implemented flexible variance thresholds to maintain tight control over cash flow. For instance, during tax season, his company enforces a strict variance threshold of less than 1%, while allowing a 3–4% variance during quieter periods.

For SMEs operating internationally, managing foreign exchange volatility is critical. Noemi Pohrib, owner of Qualiplant, turned to the iBanFirst platform to handle multiple currencies. This approach improved her company’s cash flow visibility, reduced FX conversion costs, and made payment timelines more predictable.

Seek Expert Advice

While automated tools are invaluable, external expertise can add another layer of precision to your forecasts. Advisors often spot issues or opportunities you might overlook. With experience across various industries, they can help refine your assumptions, uncover hidden cash drains, and stress-test your forecasts in practical ways.

If you’re managing a team of 15–40 people and grappling with challenges like digital transformation or go-to-market strategies, consider working with advisors like Growth Shuttle. They offer monthly asynchronous support, acting as a strategic partner to help you turn forecasting into a competitive edge.

Vinay Kevadia, Founder and CEO of Upmetrics, emphasizes the importance of this approach:

"Without clear visibility into cash inflows and outflows, strategic decisions risk being made on unstable foundations".

How to Improve Cash Flow Forecasting

Refining your cash flow forecasting process can make a big difference in how well you manage your business finances. A more accurate forecast means better decisions and less financial stress. Here’s how to fine-tune your approach and gain a competitive edge.

Monitor Key Financial Metrics

Keeping an eye on critical financial metrics is essential for creating reliable forecasts. For instance, Operating Cash Flow (OCF) shows whether your core operations generate enough cash to sustain your business. A good benchmark is maintaining an OCF margin between 10% and 20% of revenue.

Days Sales Outstanding (DSO) measures how quickly you collect payments after making a sale. For SaaS companies, the median DSO is about 45 days. If your DSO is much higher, it could point to a systemic delay in cash flow. Similarly, Days Payable Outstanding (DPO) tracks how long you take to pay your creditors. Strategically extending DPO can help preserve cash without straining relationships.

The Cash Conversion Cycle (CCC) ties these metrics together, giving you a snapshot of how long your cash is tied up in operations. It’s calculated as:

Days Inventory Outstanding + Days Sales Outstanding – Days Payable Outstanding.

If a large portion of your revenue comes from just a handful of customers – say, your top five clients account for over 40% – your cash flow risk increases.

One way to stay ahead is by using 13-week rolling forecasts, updated weekly. This approach provides a clear view of upcoming obligations like payroll, vendor payments, and collections. It forces you to address current realities instead of relying on outdated assumptions.

By tracking these metrics and updating forecasts regularly, you can better manage both receivables and payables.

Set Clear Policies for Receivables and Payables

Customer payment assumptions often don’t match reality. To improve accuracy, assign probability-based collection rates to receivables. For example, you might forecast an 85% collection rate for current invoices but only 20% for those over 90 days past due.

On average, small businesses carry around $17,500 in unpaid invoices at any time. Tightening your collection process can free up a lot of cash. Actively negotiate payment terms – aim for Net 15 or Net 30 from customers while pushing for Net 45 or Net 60 with suppliers. This strategy reduces idle funds and bridges cash gaps.

When managing payables, record outflows only when the money actually leaves your account. This prevents unexpected overdrafts. Categorize expenses into clear groups like fixed recurring costs (e.g., rent, salaries), variable recurring costs (e.g., utilities, commissions), periodic lump sums (e.g., quarterly taxes), and growth-related spending (e.g., new hires, equipment).

If you operate internationally, account for settlement delays of 2–5 business days for cross-border payments. Also, consider potential exchange rate shifts. For example, a 50-basis-point movement on a $5,000 payment could cost you $25. Over 1,000 transactions, that adds up to $25,000.

Work with Business Advisors

Bringing in external advisors can help you shift from reactive to proactive planning. They can identify hidden cash drains, challenge your assumptions, and validate your forecasts under real-world conditions.

Advisors often use techniques like probability weighting. For example, if a contract has a 70% chance of renewal, they might include only 70% of its value in your forecast to keep projections realistic.

For small to medium-sized businesses with teams of 15–40 people, services like Growth Shuttle offer tailored support. Their plans range from $600 per month for strategic calls to $7,500 per month for more in-depth, weekly guidance. They can help with challenges like digital transformation, refining market strategies, or building stronger financial processes.

When paired with financial tools, expert advice ensures consistent forecasting accuracy. Banks and lenders often view disciplined forecasting as a sign of reduced risk and greater reliability. Beyond improving internal planning, working with advisors can also enhance your credibility when seeking financing or investment.

Conclusion

Key Takeaways

For small and medium-sized enterprises (SMEs), mastering cash flow forecasting isn’t just helpful – it’s essential for staying afloat. Here’s a startling fact: 82% of small businesses fail because of poor cash flow management. It’s not about profitability; it’s about managing the actual movement of cash. That’s why focusing on when money actually enters and exits your accounts, rather than relying on invoice dates, is crucial.

Using a combination of forecasting methods can improve both short-term and long-term financial planning. The Direct Method offers a detailed view of daily cash movements, making it ideal for managing immediate needs like payroll and vendor payments over the next 1–3 months. Meanwhile, the Indirect Method is better for long-term planning and creating reports for investors. Many SMEs find success by using both: a 13-week rolling forecast for short-term liquidity and a 12-month strategic forecast for growth planning.

Another smart strategy? Scenario planning. By modeling base, optimistic, and pessimistic cases, you can prepare for unexpected events – like a client delaying payment or a supplier increasing prices. Updating forecasts weekly can make a huge difference. Research shows that weekly updates improve accuracy by 40% and reduce stress. Even dedicating just two hours a week to your forecast can save you from weeks of financial headaches.

It’s also critical to monitor key metrics like Days Sales Outstanding (DSO) and the Cash Conversion Cycle (CCC). For instance, SaaS companies typically report a median DSO of around 45 days. If your DSO is much higher, it might indicate that collections are lagging. Automating data collection through accounting software can also reduce errors, as manual spreadsheets have an error rate of up to 88%.

These insights aren’t just theory – they’re actionable steps you can take now.

Next Steps for SMEs

Ready to strengthen your cash flow management? Here’s how to get started:

- Gather key documents like bank statements, payroll records, and receivables/payables.

- Create a 13-week forecast that reflects your actual starting cash balance and realistic cash inflows – not just when payments are "supposed to" arrive.

Next, build a cash reserve. Aim for 1–2 months of operating expenses, with an additional 10–20% contingency. Commit to a weekly review – Monday mornings are a great time – to update the previous week’s actuals and adjust your forecast window forward. This routine will help you spot cash gaps 6–8 weeks ahead, giving you time to act – whether that means speeding up collections, delaying non-essential expenses, or securing financing.

If your business is navigating digital transformation or other strategic challenges and you manage a team of 15–40 people, consider partnering with Growth Shuttle. They offer expert guidance, with advisory plans ranging from $600 per month for monthly calls to $7,500 per month for weekly support. Their services can help shift your approach from reactive problem-solving to proactive planning.

At the end of the day, the businesses that succeed aren’t necessarily the most profitable – they’re the ones that always have cash on hand. Cash flow is king.

FAQs

What’s the fastest way to start a 13-week cash flow forecast?

To get started with a 13-week cash flow forecast, begin by listing all your anticipated cash inflows (like sales and receivables) and cash outflows (such as payroll and rent) for the next 13 weeks. Use a simple spreadsheet or a ready-made template to organize this information.

Make it a habit to update the spreadsheet weekly with actual numbers. This straightforward process helps you spot potential cash shortages or surpluses early, allowing you to make smarter financial decisions without unnecessary delays.

How do I forecast cash when customer payments are unpredictable?

To manage cash flow when customer payments are unpredictable, start by examining past payment trends. Look for patterns in delays to help estimate future cash inflows. It’s also wise to include a buffer in your forecast to account for late payments. Additionally, scenario planning can be a game-changer – prepare for the best-case, worst-case, and most-likely situations. By regularly updating your forecast with real payment data, you can refine its accuracy and stay on top of your cash flow management.

When should an SME use the direct method vs. the indirect method?

SMEs can benefit from using the indirect method when preparing high-level cash flow reports for stakeholders such as boards or auditors. This approach begins with net profit and adjusts for non-cash items and changes in working capital, providing a broader financial overview.

On the other hand, the direct method works best for short-term forecasting and detailed cash management. By directly recording receipts and payments, it offers a clearer picture of the timing and flow of cash.

In short, use the indirect method for strategic purposes and the direct method for day-to-day operations.

Related Blog Posts

- Scenario Analysis Methods for SMEs

- How to Build a Budget for SME Growth

- Scenario Analysis vs. Sensitivity Analysis: Key Differences

- How Demand Forecasting Reduces Supply Chain Costs

The post Ultimate Guide to Cash Flow Forecasting for SMEs appeared first on Growth Shuttle.